0

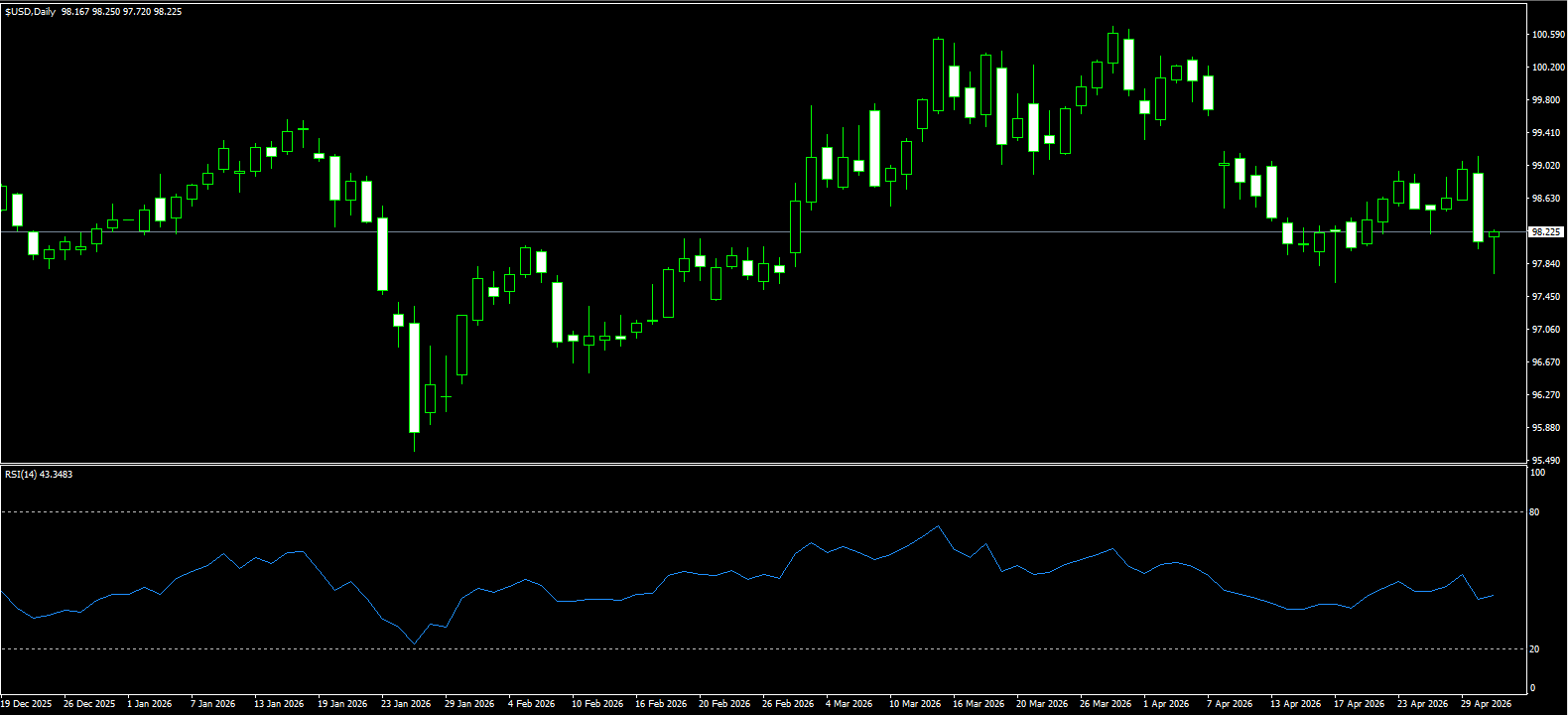

US Dollar Index (DXY)

The US Dollar Index briefly fell below the 98.00 level ahead of last weekend, after previously rebounding to a near three-week high around 99.10. The decline was largely driven by a sharp appreciation in the Japanese yen, amid suspicions of intervention by Japanese authorities in the FX market. Reports indicated that US officials had prior knowledge of the move, consistent with the G7 consensus that major currency interventions are typically communicated among member states.

On the macro front, recent data showed the US economy grew at an annualized rate of 2% in Q1, rebounding from the slowdown caused by the government shutdown at the end of 2025. Consumer spending rose 1.6%, supported by resilient services demand, while separate labor data showed jobless claims falling to multi-decade lows. Following these releases, the Federal Reserve kept interest rates unchanged, although policymakers acknowledged growing internal divisions as uncertainty tied to the Middle East conflict persists.

Heading into the weekend, the dollar regained some positive momentum, partially reversing the sharp pullback from its three-week high just above 99.10. It maintained modest gains during the European session. Against the backdrop of stalled US-Iran peace talks, President Donald Trump stated that the US would continue its maritime blockade of Iran until an agreement addressing nuclear concerns is reached. Reports that the US is considering fresh military action have further heightened tensions, adding to safe-haven demand for the dollar alongside the Fed’s hawkish bias.

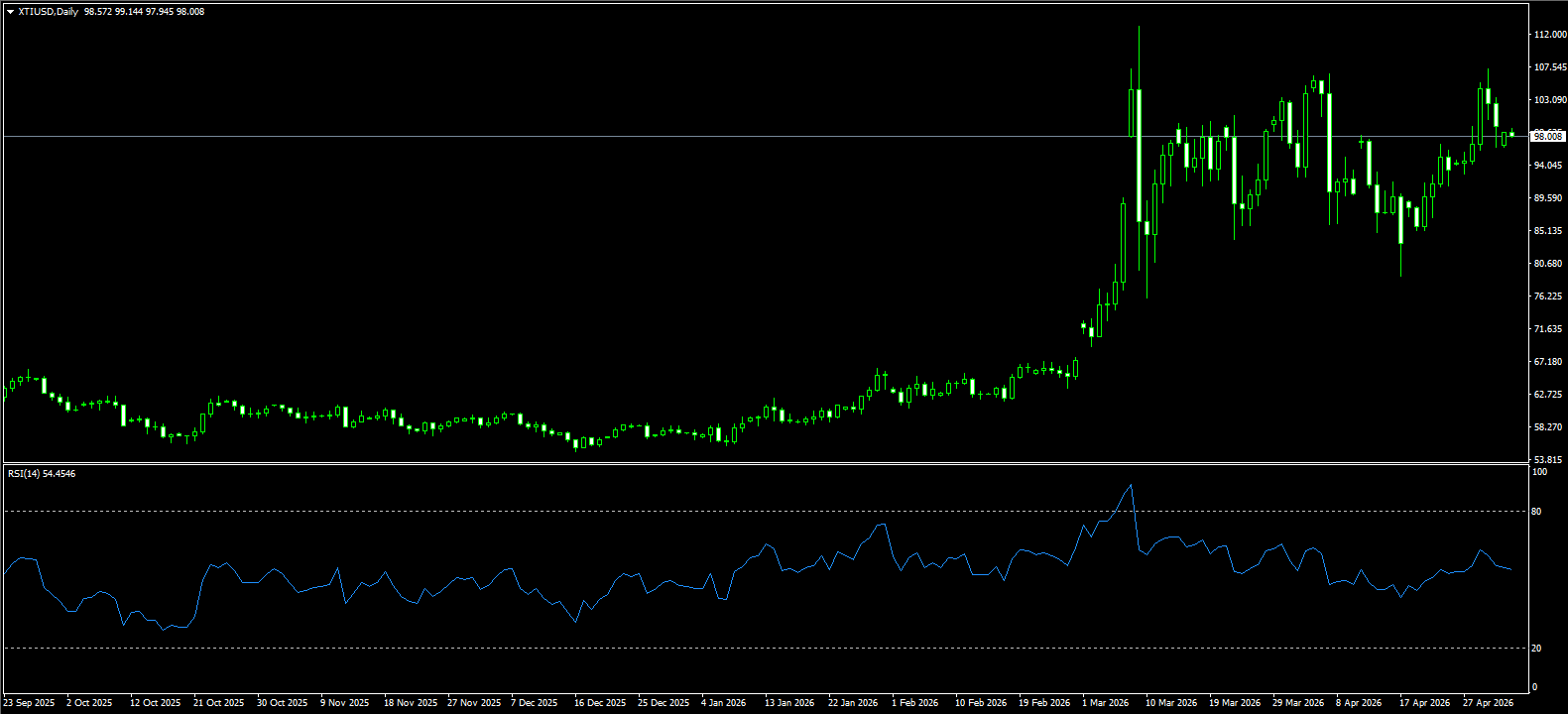

WTI Crude Oil (Spot)

WTI crude climbed back above $100 per barrel last week and is on track for a second consecutive weekly gain, driven by fading prospects for a US-Iran peace deal and expectations that the Strait of Hormuz will remain closed in the near term. Additional supply concerns emerged after the UAE’s exit from OPEC, raising the likelihood of a retest of recent highs.

President Trump reiterated that the US would maintain its maritime blockade of Iranian ports to increase economic pressure. Iran’s Supreme Leader, Mojtaba Khamenei, downplayed the chances of a deal, vowing not to abandon nuclear or missile capabilities and stating that Tehran would continue to control the strait. Meanwhile, analysts warn that several countries could soon face severe oil shortages, as the last shipments from the Persian Gulf have already reached their destinations.

Last week, US crude exports surged to record levels, as global buyers increasingly turned to US producers to offset Middle East supply disruptions. However, prices pulled back to around $99.55 ahead of the weekend, trimming weekly gains as investors grew cautiously optimistic that a fragile ceasefire could lead to lasting peace. The US has received an updated peace proposal from Iran, with Trump noting some progress but uncertainty over a final outcome.

At the same time, Trump faces a 60-day War Powers deadline regarding potential military action against Iran. Under US law, troops must be withdrawn within 60 days unless Congress authorizes deployment, and no such authorization has been granted. The administration stated that the ceasefire reached three weeks ago has effectively “ended” hostilities. Since the conflict began on February 28, oil prices have surged nearly 60%, with the closure of the Strait of Hormuz disrupting roughly one-fifth of global oil flows.

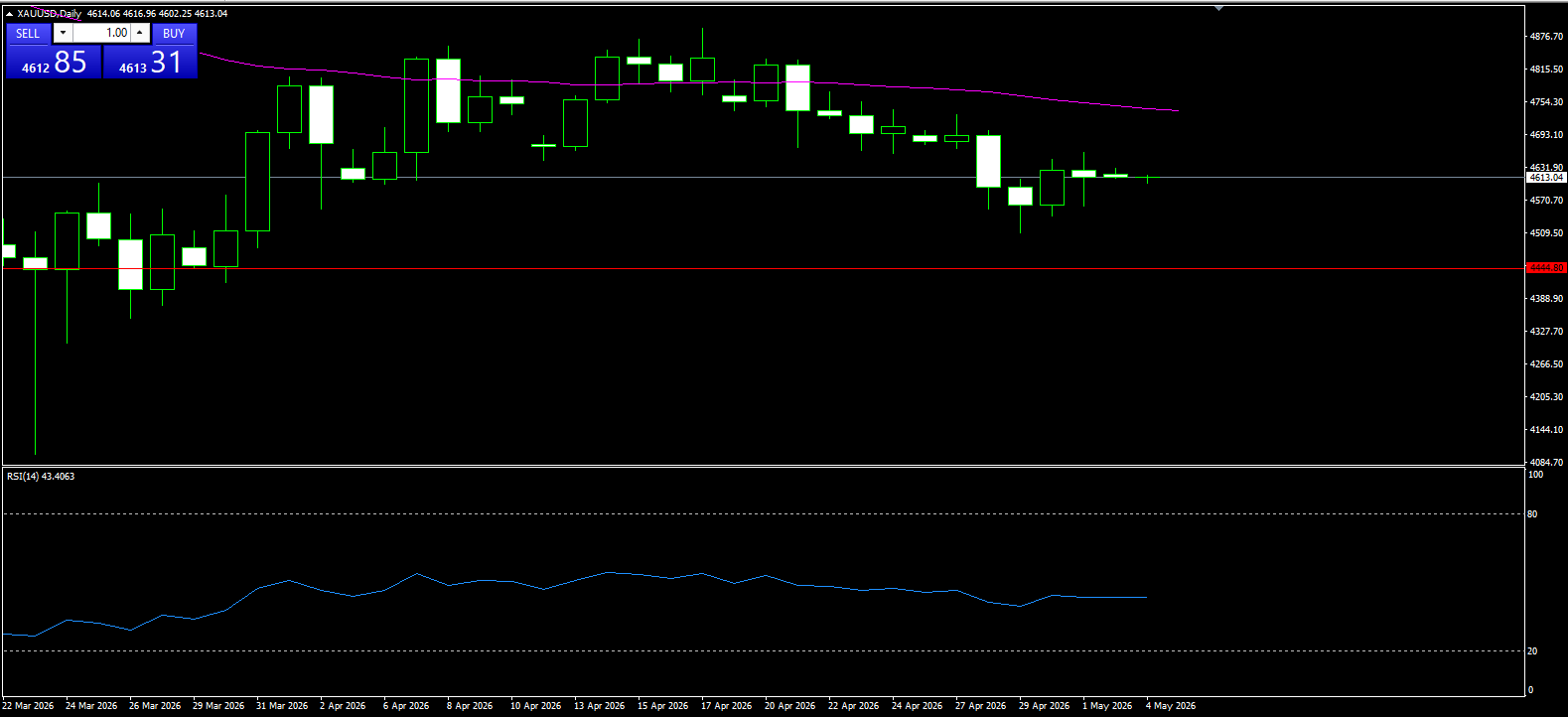

Spot Gold

On the last trading day of April, gold rose on the back of a weaker US dollar and easing oil prices, although it still posted a second consecutive monthly decline of about 1%.

Geopolitical tensions and the closure of the Strait of Hormuz have disrupted global energy supply, driving inflation sharply higher and forcing major central banks to maintain a hawkish stance. Elevated interest rates have reduced gold’s appeal. In the short term, gold is expected to remain under pressure, though the medium-term outlook remains bullish, with targets as high as $5,000.

Intraday, gold saw sharp volatility, plunging from a high near $4,700 to a one-month low around $4,510 before rebounding. This reflects the current complex interplay of geopolitics and macroeconomics: a weaker dollar and cooling oil prices provide short-term support, while inflation concerns and persistently high interest rates weigh on gold’s safe-haven appeal.

Last week, spot gold showed a pattern of “initial weakness followed by recovery,” with wide fluctuations. It remains in a medium-term corrective phase after pulling back from recent highs. Despite short-term selling pressure, the medium-term outlook remains constructive. Heightened uncertainty in the Middle East may continue to pressure gold in the near term, but it is expected to eventually regain its safe-haven appeal.

Technically, after three consecutive bearish sessions, gold formed a bullish “morning star” pattern, suggesting a short-term rebound attempt. However, it remains within a correction channel from the April 17 high of 4,890. The 5-, 10-, and 20-day moving averages are still in bearish alignment, with resistance overhead, while the 5-day MA around 4,611.90 has turned into near-term support.

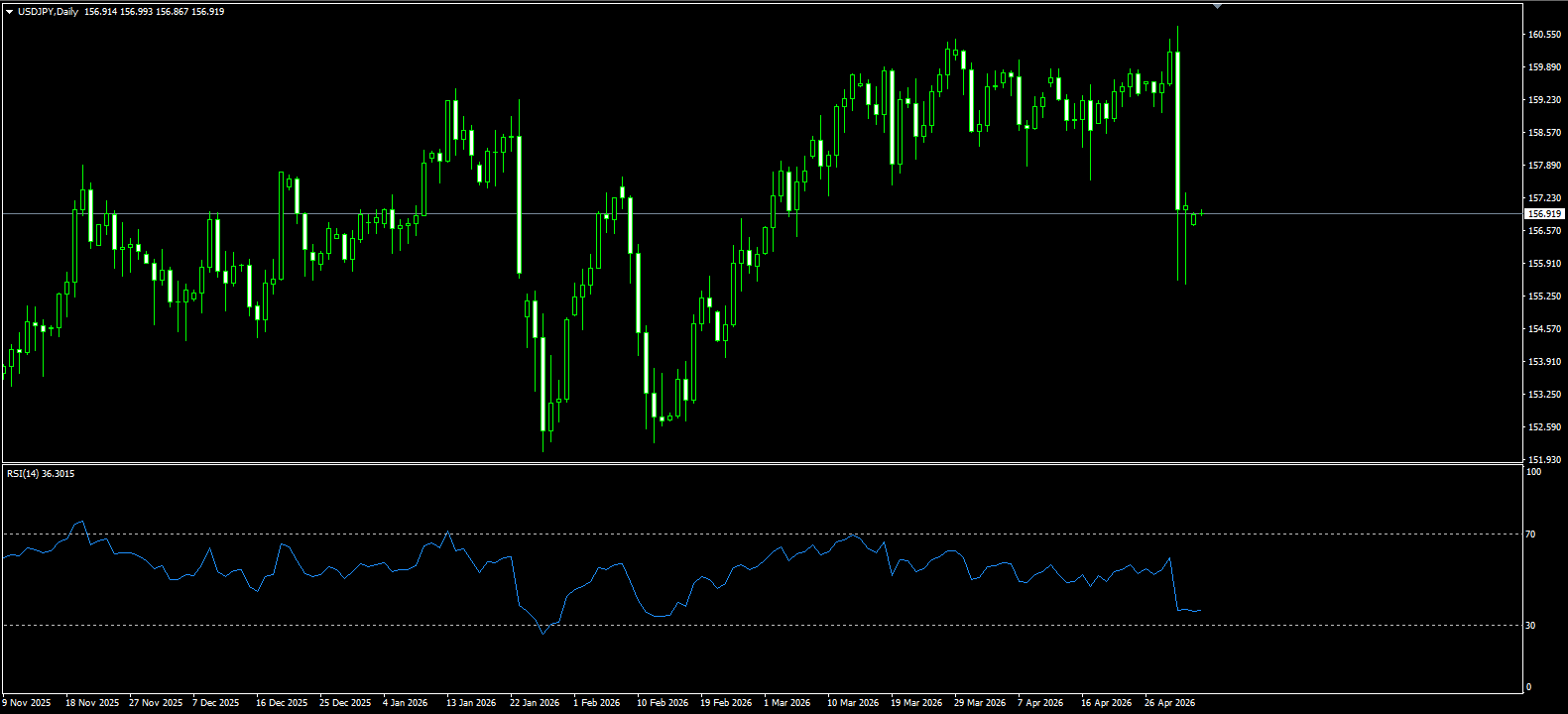

USD/JPY

USD/JPY experienced unusually sharp volatility late last week during the Asian session. After hitting a weekly high of 160.72, it plunged more than 500 pips to a low near 155.50, before stabilizing around 157. The move followed strong warnings from Japanese officials, triggering speculation of potential intervention.

Japan’s Finance Minister signaled that the time for “decisive action” was approaching, while senior currency diplomat Atsushi Mimura issued a “final warning” in Tokyo, emphasizing close coordination with US counterparts.

Several international institutions provided analysis, noting that while it is unclear whether actual intervention occurred, the urgency of intervention expectations increased significantly. The move appeared more like an amplified reaction to official warnings rather than direct market action, with some European and UK traders reportedly closing short yen positions ahead of holidays, triggering short covering.

With the Golden Week holiday approaching, such verbal interventions often have outsized effects under thin liquidity conditions. Historically, when USD/JPY approaches the key psychological level of 160, verbal intervention during low-liquidity periods can trigger chain reactions and short-term overshooting. The market remains uncertain, and USD/JPY is likely to enter a more pronounced corrective phase in the near term.

EUR/USD

The euro traded above $1.17 in early May, rebounding from a three-week low as markets assessed the European Central Bank’s latest policy decision and rising oil prices amid Middle East tensions.

The ECB kept rates unchanged but maintained flexibility for June and beyond, highlighting rising inflation risks alongside growth concerns. During the press conference, ECB President Christine Lagarde confirmed that the decision was unanimous, although rate hikes had been discussed. Other ECB officials warned that tightening could come as early as June, citing worsening inflation prospects. Markets are now pricing in up to three rate hikes in 2026, with the first fully priced in by July.

Meanwhile, Trump’s continued maritime blockade of Iranian ports has pushed Brent crude prices higher. However, recent ECB communication has had limited impact on euro rates and the currency itself. Markets still assign nearly a 90% probability to a June rate hike.

Oil price fluctuations have driven much of the movement in euro swap rates, and EUR/USD is expected to trade within a 1.1650–1.1800 range until greater clarity emerges on Gulf tensions. Given last week’s volatility in oil markets, it is difficult to isolate the ECB’s influence on short-term euro rates. The conclusion is that the impact has likely been limited.

That said, the ECB’s relatively firm stance helps support the euro by anchoring tightening expectations and keeping market rates sufficiently elevated, preventing an undesirable decline in real interest rates.

More Coverage

Risk Disclosure:Derivatives are traded over-the-counter on margin, which means they carry a high level of risk and there is a possibility you could lose all of your investment. These products are not suitable for all investors. Please ensure you fully understand the risks and carefully consider your financial situation and trading experience before trading. Seek independent financial advice if necessary before opening an account with BCR.

BCR Co Pty Ltd (Company No. 1975046) is a company incorporated under the laws of the British Virgin Islands, with its registered office at Trident Chambers, Wickham’s Cay 1, Road Town, Tortola, British Virgin Islands, and is licensed and regulated by the British Virgin Islands Financial Services Commission under License No. SIBA/L/19/1122.

Open Bridge Limited (Company No. 16701394) is a company incorporated under the Companies Act 2006 and registered in England and Wales, with its registered address at Kemp House, 160 City Road, London, City Road, London, England, EC1V 2NX. This entity acts solely as a payment processor and does not provide any trading or investment services.

English

English

简体中文

简体中文

繁體中文

繁體中文

Bahasa

Melayu

Bahasa

Melayu

Tiếng

Việt

Tiếng

Việt

ไทย

ไทย

日本語

日本語

한국어

한국어

ភាសាខ្មែរ

ភាសាខ្មែរ

español

español